After nearly two years of declining volumes, that’s the kind of signal distributors, OEMs, and contractors have been waiting for. But before the industry breathes a collective sigh of relief, it’s worth looking closely at what that claim actually means — and what it doesn’t.

Because later in the same report is a more important point: Stopping the decline is not the same thing as starting a recovery.

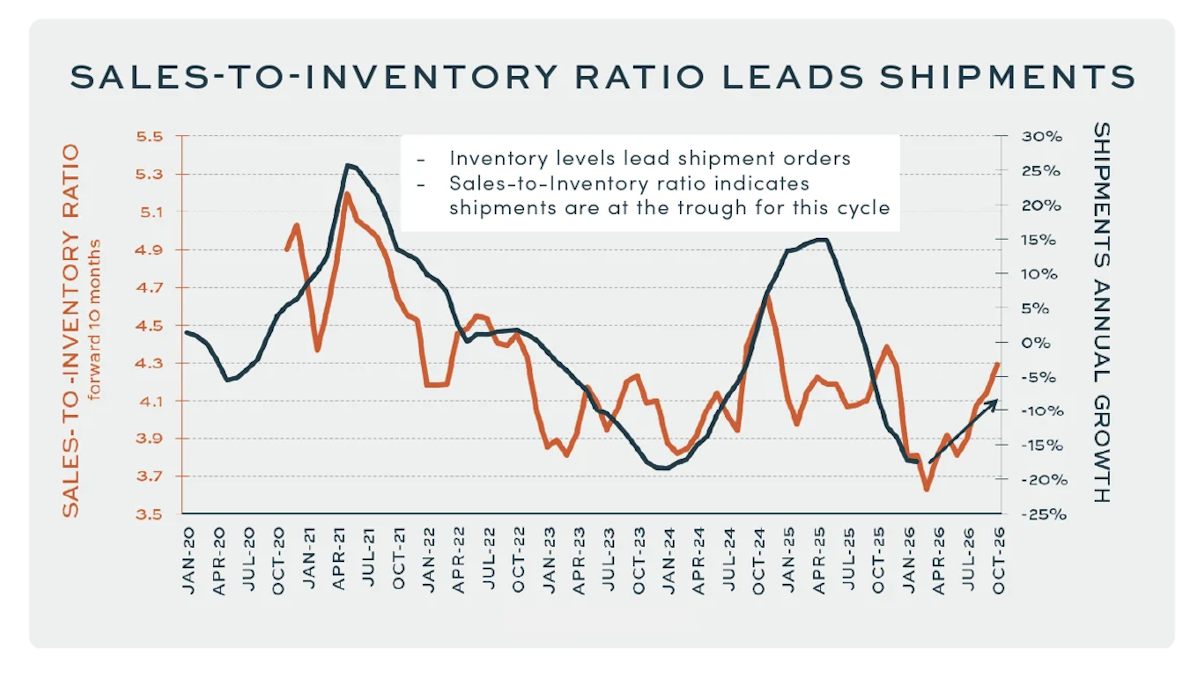

What It Means To Be At A Shipment Bottom

A shipment “bottom” typically reflects a shift in channel behavior, not necessarily a surge in customer demand.

After an extended period of destocking, distributors eventually reach a point where they simply can’t reduce inventory any further. Orders begin to align more closely with actual sales, and shipment declines moderate.

That appears to be where the industry is now. After the over-ordering of 2021-2022 and the aggressive destocking that followed due to the refrigerant transition, HARDI’s analysis suggests the system is starting to normalize.

OUT OF THE SLUMP: HARDI’s analysis suggests the annual growth rate of shipments (the dark line) is about to turn higher to follow the orange sales-to-inventory ratio line. (Courtesy of AHRI)

“The first step toward understanding shipment demand is measuring the amount of inventory distributors have,” HARDI writes, referring to data from AHRI. “We moved the orange line forward until we found the best fit with the annual growth rate of shipments. That relationship was ten months, and indicates the annual growth rate of shipments, the dark line, is about to turn higher to follow the orange sales-to-inventory ratio line.”

Looking for quick answers on air conditioning, heating and refrigeration topics?

Try Ask ACHR NEWS, our new smart AI search tool.

Ask ACHR NEWS

That’s what a shipment bottom really signals: The end of the correction phase. The good news is, the industry stops falling — but so far, it’s still just a supply chain milestone.

End Market Demand Is The Real Test

HARDI is right to separate “end market demand” as the second step. That’s where the real question lies for the rest of 2026.

For these answers, HARDI is focusing on two main factors. First up: Temps.

“Warmer weather will melt the elevated distributor inventories toward normal levels,” HARDI said — and it’s true: Warmer-than-normal average temps in March likely provided an early boost to seasonal demand this year.

The second factor is home sales. After a 30-month rate tightening cycle, existing home sales have been near 4 million for more than two years, HARDI pointed out. For comparison, the last time home sales were at this level was a four-month period during the Great Recession.

“This extended period of depressed housing activity is one reason that we have been through our recession,” HARDI wrote. “The only question for us is when will demand improve?”

Meanwhile, 30-year mortgage rates, after a temporary dip to below 6%, are back up to 6.4%, driven by inflation expectations.

Pricing Still Clouds The Picture

There’s another layer complicating all of this: pricing.

Over the past several years, inflation has masked weaker unit volumes across the HVAC industry. Revenues have held up better than shipments, but that doesn’t necessarily mean demand is healthy — it may just mean everything costs more. And manufacturers have made it clear they don’t expect prices to come back down.

That raises a more uncomfortable question: Is HVAC demand actually going to strengthen, or is it simply going to stabilize at a lower level?

Contractors are already feeling that tension. One emailed The ACHR NEWS recently with a blunt assessment: Electrification and efficiency are important, but affordability is becoming the real issue.

“I’ve had customers crying saying that they can’t afford new heating and cooling,” he told us.

Lennox reported in a recent earnings call that minimum-SEER equipment now accounts for roughly 70% of the company’s sales, and I’m not surprised. High prices and broader economic uncertainty make people hesitant on big purchases.

On that second point, HARDI doesn’t disagree.

“Our hopes for improving demand this year as inflation subsided has been dimmed by the uncertainty associated with current events … With the commodity costs spiking and trying to decide if the rapid roll-out of AI is a threat or opportunity, ‘uncertainty’ may be the most appropriate word for today.”

Stability Vs. Strength

If HARDI’s data proves right, the industry may finally be through the worst of the inventory correction. The freefall is likely behind us, and the numbers should start to look more stable.

But stability is not the same as strength.

What happens next won’t be driven by distributor behavior or shipment math. It will be decided in living rooms and at kitchen tables, where homeowners are weighing high interest rates, rising costs, and whether they can afford to replace a system at all.

That’s the part of the recovery no dataset can model cleanly. If pricing outpaces what consumers are willing — or able — to pay, demand doesn’t snap back. It plateaus. That’s a very different kind of “recovery” than the industry is used to.

Whether you require installation, repair, or maintenance, our technicians will assist you with top-quality service at any time of the day or night. Take comfort in knowing your indoor air quality is the best it can be with MOE heating & cooling services Ontario's solution for heating, air conditioning, and ventilation that’s cooler than the rest.

Contact us to schedule a visit. Our qualified team of technicians, are always ready to help you and guide you for heating and cooling issues. Weather you want to replace an old furnace or install a brand new air conditioner, we are here to help you. Our main office is at Kitchener but we can service most of Ontario's cities

Source link